.

Agentic AI Resources

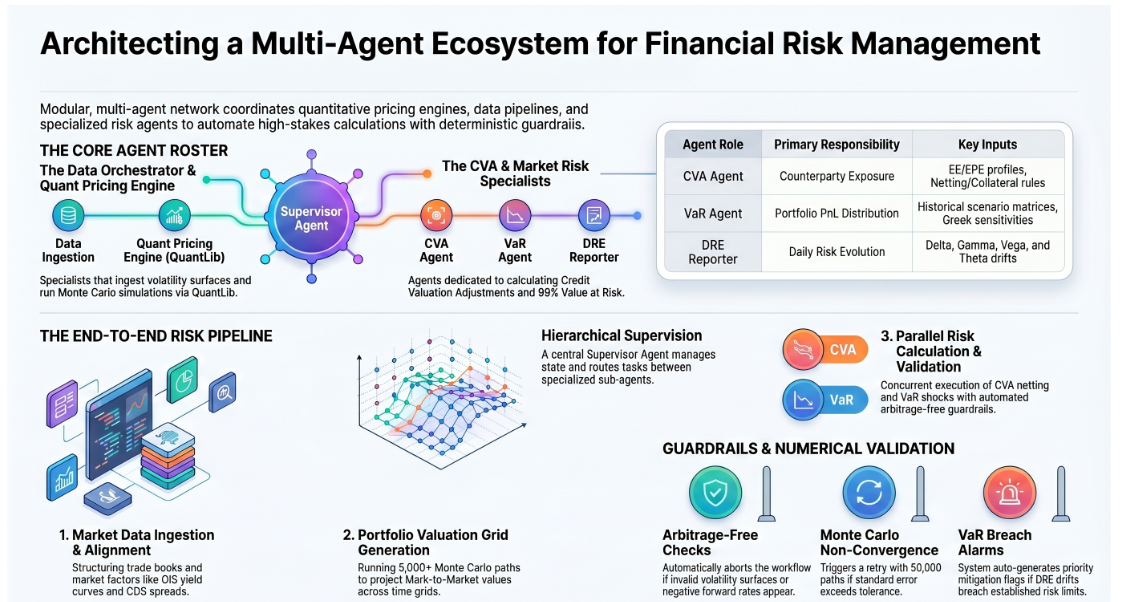

Multi-agent systems improve the precision of Credit Valuation Adjustment (CVA) and Value at Risk (VaR) by replacing monolithic processing with a modular, specialized architecture that incorporates automated guardrails, deterministic loops, and sophisticated data validation.

1. Automated Convergence Guardrails: One of the primary ways precision is improved is through Supervisor Agents that enforce strict numerical validation rules.

For instance: Monte Carlo Precision: If a path simulation fails a standard error tolerance (SE>ϵ), the system automatically retries with a higher seed path count (e.g., increasing N to 50,000) to ensure convergence.Loop-Back Logic: Frameworks like LangGraph enable "deterministic state transitions." If a pricing simulation fails validation, the system reroutes the data upstream for recalculation rather than allowing "bad data" to reach risk dashboards.

2. Specialized Domain Expertise :By dividing labor among specialized agents, the system mimics a professional quantitative risk desk, ensuring each component is handled by a "master" of that specific domain:

Data Orchestrator Agent: Improves precision by running Arbitrage-Free Checks. It ensures that yield curves and volatility surfaces are economically valid before they are used in calculations, aborting the workflow if invalid data is detected.

Quant Pricing Agent: Uses industry-standard tools like QuantLib to run high-performance Monte Carlo simulations (e.g., Hull-White or Black-Scholes) to generate future Mark-to-Market (MtM) paths.

CVA Specialist Agent: Increases accuracy by applying legal netting rules and Credit Support Annex (CSA) collateral agreements at the netting-set level, ensuring positive and negative exposures are offset correctly according to Basel standards.

3. Enhanced Sensitivity Calculations :Multi-agent systems improve VaR and Daily Risk Evolution (DRE) precision by refining how sensitivities (Greeks) are measured:

Stable Greek Attribution: Instead of relying on potentially unstable finite-difference calculations, agents can isolate exact Greek parameters (Delta/Vega shifts) by comparing valuation matrices across consecutive dates.

Multi-Factor Risk Attribution: The system independently processes historical shocks across different asset classes and currencies, accurately isolating how specific market movements and time decay (Theta) impact the portfolio.

4. Shared State and Parallelism : The use of a shared-state ledger (like a RiskEngineState) ensures that all agents—whether calculating CVA or VaR—ingest the exact same immutable valuation matrix simultaneously. This eliminates serialization errors and ensures that different risk metrics are perfectly aligned and derived from the same underlying simulation data.

Pleasantview Gem Inn

Not just pleasant on the outside, our Pleasantview Gem Inn properties are especially popular among families. With underground parking and floor-to-ceiling windows, there's no shortage of natural light or space.